Closing Costs! What You Should Know

What You Should Know About Closing Costs Before you buy a home, it’s important to plan ahead. While most buyers consider how much they need to save for a down payment, many are surprised by the closing costs they have to pay. To ensure you aren’t caught off guard when it’s time to close on your home

Top 5 Monmouth County Beaches

Top 5 Monmouth County Beaches Monmouth County is known for its breathtaking beaches and is a popular destination for beachgoers. Here are some of the best beaches in Monmouth County, NJ that you should consider visiting: 1. Seven Presidents Oceanfront Park: This park is named after the seven Unit

Experts Can Help Close the Gap in Today’s Homeownership Rate

How Experts Can Help Close the Gap in Today’s Homeownership Rate As we celebrate Black History Month, we reflect on the past and present experiences of Black Americans. This includes the path toward investing in a home of their own. And while equitable access to housing has come a long way, homeowne

This Spring: The Top Reasons for Selling Your House

The Top Reasons for Selling Your House Caption Many of today’s homeowners bought or refinanced their homes during the pandemic when mortgage rates were at history-making lows. Since rates doubled in 2022, some of those homeowners put their plans to move on hold, not wanting to lose the low mortg

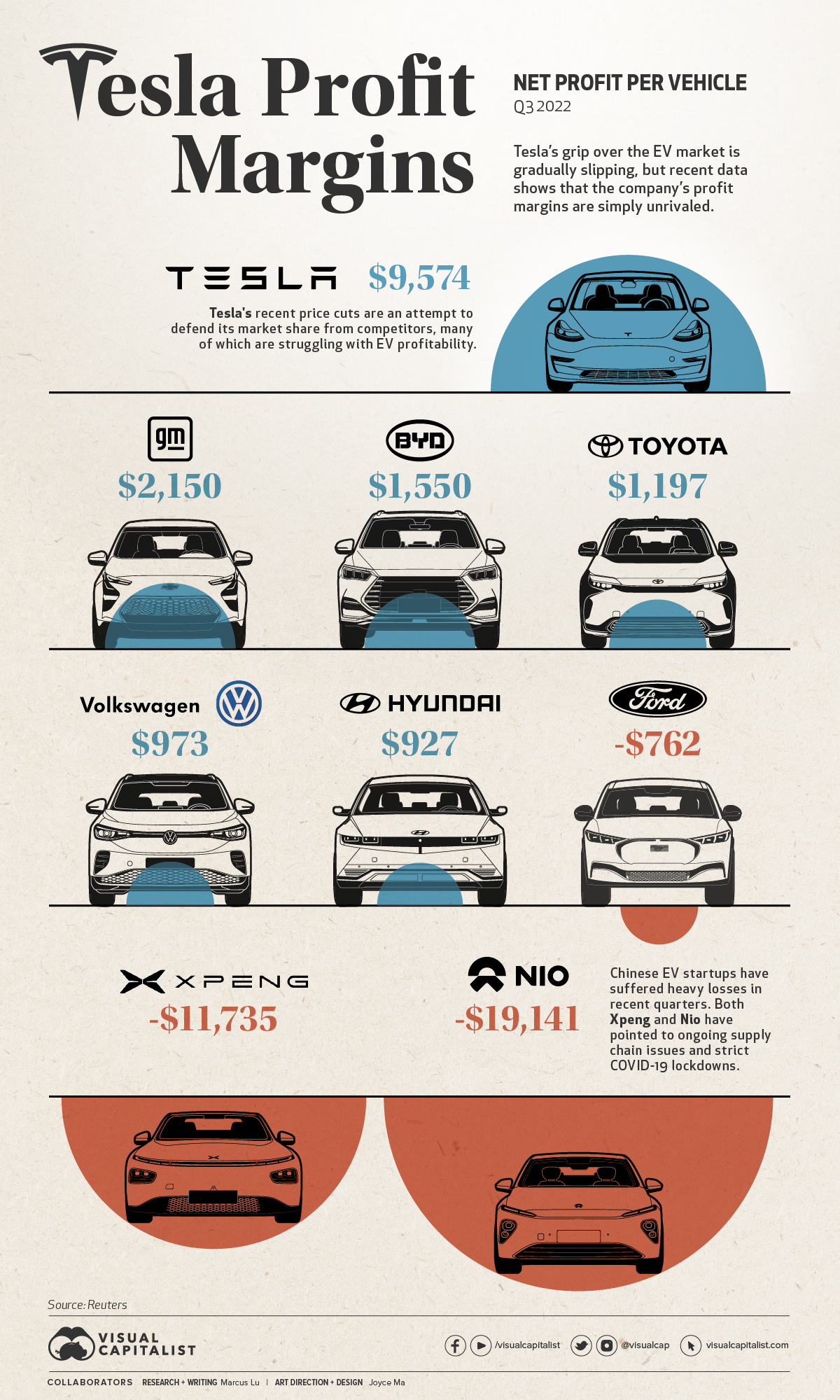

Tesla’s Unrivaled Profit Margins

Chart: Tesla’s Unrivaled Profit Margins In January this year, Tesla made the surprising announcement that it would be cutting prices on its vehicles by as much as 20%. While price cuts are not new in the automotive world, they are for Tesla. The company, which historically has been unable to kee

The Top House-Hunting Mistakes We See

Caption Buying a home is a very emotional process. If you allow those emotions to get the best of you, you may fall prey to several common home buyer mistakes. Since homeownership has far-reaching implications, it's important to keep your emotions in check and make the most rational decision possibl

Home Prices Are Slightly Lower, But Far From Plummeting

30YR Fixed 6.16% -0.01% 15YR Fixed 5.23% -0.01% Home Prices Are Slightly Lower, But Far From Plummeting As rates spiked and sales contracted at the fastest pace in decades last year, we knew the post-pandemic surge in home prices was set to reverse. By the middle of 2022, the average forecast saw

Lower Mortgage Rates Are Bringing Buyers Back to the Market

Lower Mortgage Rates Are Bringing Buyers Back to the Market As mortgage rates rose last year, activity in the housing market slowed down. And as a result, homes started seeing fewer offers and stayed on the market longer. That meant some homeowners decided to press pause on selling. Now, however, ra

Where Will You Go If You Sell? We Have Options

There are plenty of good reasons you might be ready to move. No matter your motivations, before you list your current house, you need to consider where you’ll go next. In today’s market, it makes sense to explore all your options. That includes both homes that have been lived in before as well as

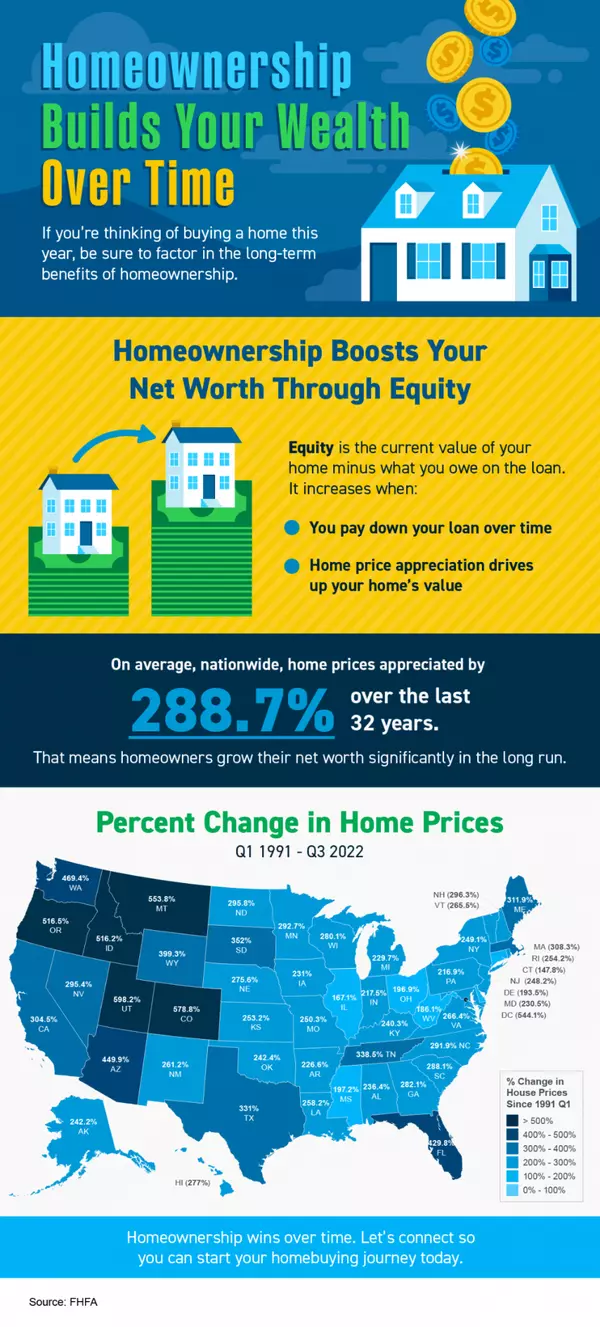

Homeownership Builds Your Wealth Over Time

Some Highlights If you’re thinking of buying a home this year, be sure to factor in the long-term benefits of homeownership. On average, nationwide, home prices appreciated by 288.7% over the last 32 years. That means homeowners grow their net worth significantly in the long term. Homeownership wins

New Home Sales Look Like They Want to Bounce

New Home Sales Look Like They Want to Bounce The Census Bureau's regularly scheduled monthly report on New Home Sales was released this morning. The annual pace of 616k was right in line with the median forecast of 617k. This is technically an improvement, but only because the previous month was r

At The Shore, It Can Make Sense To Move Before Spring

Spring is usually the busiest season in the New Jersey and Monmouth County housing market. Many buyers wait until then to make their move, believing it’s the best time to find a home. However, that isn’t always the case when you factor in the competition you could face with other buyers at that ti

Why Pricing Your House Appropriately Matters

Why Pricing Your House Appropriately Matters Last year, the housing market slowed down in response to higher mortgage rates, and that had an impact on home prices. If you’re thinking of selling your house soon, that means you’ll want to adjust your expectations accordingly. As realtor.com explains:

Rates May be Falling, But Other Mortgage Costs Are Going Up

Rates May be Falling, But Other Mortgage Costs Are Going Up Mortgage rates have fallen quite a bit since hitting a long term peak in late October. By the middle of this week, the average 30yr fixed rate was more than 1.25% lower from the highs and at the best levels in more than 4 months. Rates ha

Existing Home Sales Shrink for 11th Month

30YR Fixed 6.11% +0.07% 15YR Fixed 5.15% +0.03% Existing Home Sales Shrink for 11th Month Existing home sales fell back for the 11th straight month in December according to the National Association of Realtors® (NAR) The month’s sales of pre-owned single-family houses, townhouses, condominiums, an

Mortgage Pre-Approval in 2023: One Of The First Steps

Pre-Approval in 2023: What You Need To Know One of the first steps in your homebuying journey is getting pre-approved. To understand why it’s such an important step, you need to understand what pre-approval is and what it does for you. Business Insider explains: “In a preapproval [sic], the lender t

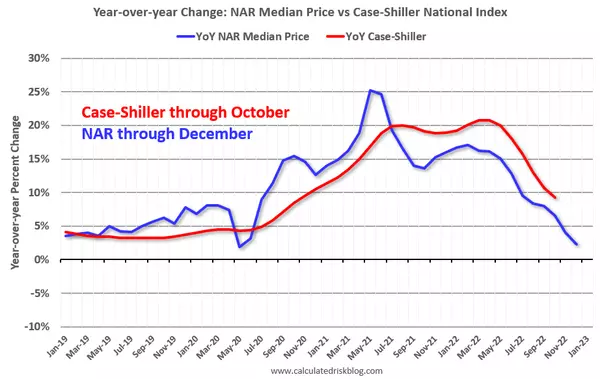

Have Home Values Hit Bottom?

Have Home Values Hit Bottom? Whether you’re already a homeowner or you’re looking to become one, the recent headlines about home prices may leave you with more questions than answers. News stories are talking about home prices falling, and that’s raising concerns about a repeat of what happened to p

Builders See a Turn-Around in Housing Starts on the Horizon

30YR Fixed 6.04% -0.13% 15YR Fixed 5.12% -0.16% Builders See a Turn-Around in Housing Starts on the Horizon On top of the solid report on mortgage volume earlier today, comes another hopeful report from the construction industry. The National Association of Home Builders (NAHB) says builder confid

Lower Inflation Portends Further Slide in Mortgage Rates

A dip below 6% has become a distinct possibility, says NAR Chief Economist Lawrence Yun. Inflation has been dropping over the past six months, and consumers can expect mortgage rates to soon follow, says Lawrence Yun, chief economist for the National Association of REALTORS®. The 30-year fixed-rat

Ryan Skove

Phone:+1(732) 222-6336