Pending Home Sales Decline for Fifth Month in a Row

96 Ryan Skove has shared this article with you. View | Download 30YR Fixed 6.65% +0.03% 15YR Fixed 6.00% -0.02% Pending Home Sales Decline for Fifth Month in a Row October saw contracts to purchase existing homes fall for the fifth straight month. The National Association of Realtors®

3 Ways You Can Use Your Home Equity

If you’re a homeowner, odds are your equity has grown significantly over the last few years as home prices skyrocketed and you made your monthly mortgage payments. Home equity builds over time and can help you achieve certain goals. According to the latest Equity Insights Report from CoreLogic, the

Your House Could Be the #1 Item on a Homebuyer’s Wish List During the Holidays

Each year, homeowners planning to make a move are faced with a decision: sell their house during the holidays or wait. And others who have already listed their homes may think about removing their listings and waiting until the new year to go back on the market. The truth is many buyers want to purc

What Buyers Need To Know About the Inventory of Homes Available for Sale

⇒ If you’re thinking about buying a home, you’re likely trying to juggle your needs, current mortgage rates, home prices, your schedule, and more to try to decide if you want to jump into the market. If this sounds like you, here’s one key factor that could help you with your decision: there are mor

What Homeowners Want To Know About Selling in Today’s Market

If you’re thinking about selling your house, you’re likely hearing about the cooling housing market and wondering what that means for you. While it's not the peak intensity we saw during the pandemic, we’re still in a sellers’ market. That means you haven’t missed your window. Realtor.com explains:

Mortgage Rates Will Come Down, It’s Just a Matter of Time

This past year, rising mortgage rates have slowed the red-hot housing market. Over the past nine months, we’ve seen fewer homes sold than the previous month as home price growth has slowed. All of this is due to the fact that the average 30-year fixed mortgage rate has doubled this year, severely li

Fed Says: Don't Get Too Excited About Rates Just Yet

Ryan Skove has shared this article with you. View | Download 30YR Fixed 6.63% -0.02% 15YR Fixed 6.05% -0.05% Fed Says: Don't Get Too Excited About Rates Just Yet There's no question that last week was an exciting one for rates. On Wednesday, the average 30yr fixed was fairly close to the

More People Are Finding the Benefits of Multigenerational Households Today

If you’re thinking of buying a home and living with siblings, parents, or grandparents, then multigenerational living may be for you. The Pew Research Center defines a multigenerational household as a home with two or more adult generations. And the number of individuals choosing multigenerational l

Top Questions About Selling Your Home This Winte

There’s no denying the housing market is undergoing a shift this season, and that may leave you with some questions about whether it still makes sense to sell your house. Here are three of the top questions you may be asking – and the data that helps answer them – so you can make a confident decisio

Construction Costs, Buyer Traffic Continue to Sap Builder Confidence

Ryan Skove has shared this article with you. View | Download 30YR Fixed 6.64% +0.03% 15YR Fixed 6.08% +0.03% Construction Costs, Buyer Traffic Continue to Sap Builder Confidence The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) fell another 5 point

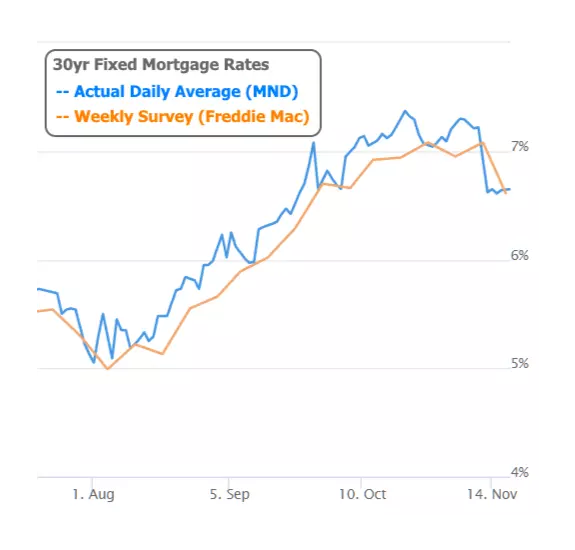

Mortgage Rates Roughly Unchanged After Last Week's Huge Drop

Ryan Skove has shared this article with you. View | Download 30YR Fixed 6.61% -0.04% 15YR Fixed 6.05% -0.07% Mortgage Rates Roughly Unchanged After Last Week's Huge Drop If you're just getting caught up, last Thursday was one for the record books--at least when it comes to the daily reco

It May Be Time To Add Newly Built Homes to Your Search

If you put a pause on your home search because you weren’t sure where you’d go once you sold your house, it might be a good time to get back into the market. If you’re willing to work with a trusted agent to consider a newly built home, you may have even more options and incentives than you realize.

What’s Ahead for Mortgage Rates and Home Prices?

What’s Ahead for Mortgage Rates and Home Prices? Now that the end of 2022 is within sight, you may be wondering what’s going to happen in the housing market next year and what that may mean if you’re thinking about buying a home. Here’s a look at the latest expert insights on both mortgage rates and

Early Indications Show September Home Prices Falling Less Than July/August

Ryan Skove has shared this article with you. View | Download 30YR Fixed 7.21% -0.04% 15YR Fixed 6.55% -0.07% Early Indications Show September Home Prices Falling Less Than July/August Roughly 2 weeks ago, home price indices (HPIs) from Case Shiller and the FHFA came out for the month of

The Majority of Americans Still View Homeownership as the American Dream

Buying a home is a powerful decision, and it remains a key part of the American Dream. In fact, the 2022 Consumer Insights Report from Mynd found the majority of people polled still view homeownership as a key life achievement. Let’s explore just a few of the reasons why so many Americans continue t

Key Factors Affecting Home Affordability Today

Every time there’s a news segment about the housing market, we hear about the affordability challenges buyers are facing today. Those headlines are focused on how much mortgage rates have climbed this year. And while it’s true rates have risen dramatically, it’s important to remember they aren’t the

3 Trends That Are Good News for Today’s Homebuyers

While higher mortgage rates are creating affordability challenges for homebuyers this year, there is some good news for those people still looking to buy a home. As the market has cooled this year, some of the intensity buyers faced during the peak frenzy of the pandemic has cooled too. Here are jus

Millennials Are Still a Driving Force of Today’s Buyer Demand

If you’re thinking about selling your house but wondering if buyers are still out there, know that there are still people who are searching for a home to buy today. And your house may be exactly what they’re looking for. While the millennial generation has been dubbed the renter generation, that nam

Fannie, Freddie ordered to slash fees for many first-time homebuyers

Regulators order mortgage giants to eliminate upfront fees on many purchase loans in order to help first-time homebuyers of limited means, the Federal Housing Finance Agency said Monday Fannie Mae and Freddie Mac’s federal regulator is ordering the mortgage giants to eliminate upfront fees on many p

3 Graphs Showing Why Today’s Housing Market Isn’t Like 2008

3 Graphs Showing Why Today’s Housing Market Isn’t Like 2008 With all the headlines and talk in the media about the shift in the housing market, you might be thinking this is a housing bubble. It’s only natural for those thoughts to creep in that make you think it could be a repeat of what took place

Ryan Skove

Phone:+1(732) 222-6336